Not certain you've read the figures properly? Or just picking out the bits that support your usual narrative?

"They always appear to me like a business in receivership, just keeping their heads above water" - you should check out the liquidity and cashflow figures. In fact, they now have a better cash flow because of the SWR franchise though, of course, that is lower margin business. I might also add that whilst you may believe that First Group have bought another year, that's handy as next year, another lump of very expensive Moir era debt falls off so they'll be able to get a better deal on that! Not withstanding the fact that group debt has dropped further - did you miss all of those figures?

In terms of UK Bus, the revenue is up by £5m but the operating profit is up by £9m. That's partly because they've been screwing down the costs. Comparing with the previous year, they have had the pain of the one offs for closing the two Manc depots and Rotherham but those revised cost bases together with improved revenue capture (basically, less fiddling by drivers) is feeding through. Of course, there are other issues like the reduced new vehicle intake (only 180 vehicles of which a number are on lease rather than capital spend) though increasing in 2018/9 to 260. Then there are like for like increases in passenger volumes of 0.7% - quite modest but compare with the industry?

Congestion is their biggest enemy and they say, clearly, that they will invest where LA stakeholders will work with them to tackle this. Put another way - if an LA isn't playing ball (take somewhere like Somerset), what do you expect them to do? Invest in levitating buses that can avoid road congestion in Taunton? Build their own bus lanes? I'd question why they'd be putting much more operational strategy detail in their half year update???

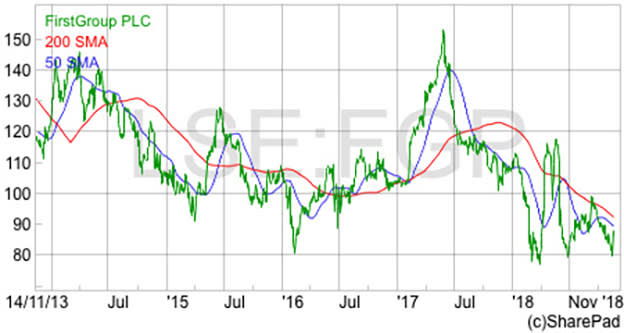

If you want to beat First Group with a stick, the absence of anything reflecting the clamour to divest from activist investors is the most obvious gap. As a shareholder, these are nothing much more than a solid set of results. Nothing transformational but heading the right way though very slowly - debt is coming down, the pension deficit cut, though no sign of a dividend or fundamental value creation. As has been said before, whether that's enough to appease investors whose patience has been sorely tried, I would doubt.

I’d .ime to take issue with your statement about drivers fiddling where is your proof, from personal knowledge this has mostly come from the introduction of Ticketer machines stopping PASSENGER fraud through screenshotted weekly and monthly tickets as well as pass misuses through sharing passes and fraudulent weekly tickets. The advent of QR codes on all tickets has reduced fraud to amazingly low levels.

Equally the accurate recording of concessionary permits has assisted with better payouts from local authorities.

So best you read some of First’s own press releases regarding the new ticketing equipments bonuses.

So maligning hard working bus drivers who have put up with sub standard equipment in the past and relying on a flash of a pass with little hope on a busy bus of pulling a fraudulent pass was impossible.